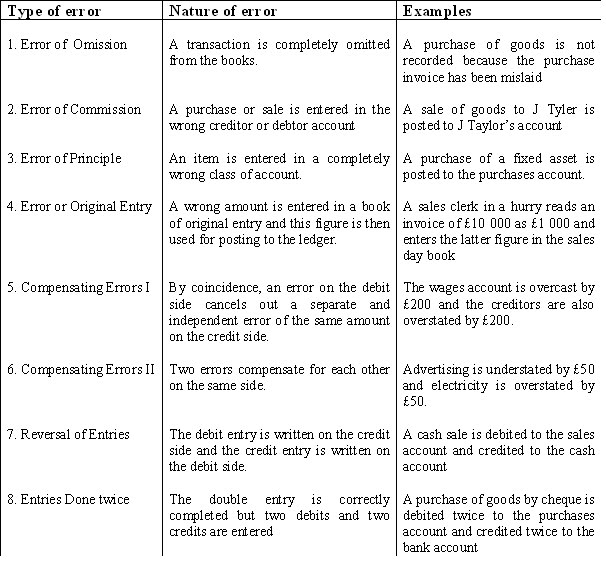

Effect of Errors on Profit or Loss

Some errors affect the profit while others do not. This distinction does not always coincide with whether or not the trial balance balances.

Errors affecting Profit or Loss

These errors affect those accounts which are included in the Trading and Profit and Loss Account eg purchases, sales, expenses etc. We must ask the following questions:

1) Does the error affect the gross profit, the net profit or both?

(a) Errors which affect items that go into the trading account affect gross profit and net profit to the same extent and in the same direction. Such items are sales, purchases, returns, stock, carriage inwards etc.

(b) Errors which affect items that are entered in the profit and loss section of the account, i.e. operating expenses, affect only net profit. Purchases of fixed assets affect profit only indirectly through provisions for depreciation.

2) In what direction is profit affected?

(a) If sales are overstated or purchases understated, both gross profit and net profit are too high and must be reduced by the relevant amount. The same applies if sales returns are understated or purchases returns overstated.

(b) If sales are understated or purchases overstated, both gross profit and net profit are too low and must be increased by the relevant amount. The same applies if sales returns are overstated or purchases returns understated.

(c) If miscellaneous receipts are overstated or if expenses are understated, gross profit is not affected but net profit will be high and must be reduced.

(d) If miscellaneous receipts are understated or if expenses are overstated, again gross profit is not affected but net profit is too low and must be increased.

(e) If capital expenditure is wrongly treated as revenue expenditure, eg if the purchase of a fixed asset is treated as an expense, then net profit will be too low and must be increased. The opposite applies if revenue expenditure is treated as capital expenditure.

3) Does the errors that affect items in the balance sheet affect profit as well? The answer is only those that were adjusted after the trial balance was prepared. Errors affecting fixed assets, current assets and liabilities do not normally affect profit but if one of these items has changed as a result of an adjustment, then profit is affected. For example:

(a) If the closing stock has been overvalued, the stock figure in the balance sheet is too high and so are the gross profit and the net profit. The opposite is true of a closing stock which is undervalued. Remember that closing stock adds on to gross profit and opening stock takes away from it.

(b) If an accrued or prepaid expense is the wrong amount, both profit and the item in the balance sheet are wrong. If an amount owing is overstated or a prepayment is understated, profit is too low and must be increased, and vice versa.

(c) The opposite to (b) applies in the case of accrued or prepaid receipts.

Estimating the effects of errors can be confusing and you must keep a clear mind. Think how the original figure has affected profit and then try to see in which direction the error is affecting the profit.

No comments:

Post a Comment